What is a Business Loan?

A business loan is borrowed loan used for business purposes, such as expansion or smoothing out cash flow fluctuations. One can obtain a business loan from a variety of sources and then repay it in monthly or quarterly installments plus interest.

How do Business Loans work?

A loan for a business requires an application and explanation of its intended use. Similar to qualifying for a personal loan, you’ll need to demonstrate to the lender that you have steady income and a plan to repay the loan.

What length of time you decide to take it out for is entirely up to you. Medium- and long-term loans often have loan terms ranging from one to thirty years. The loan’s interest rate and monthly payment are often locked in for its whole.

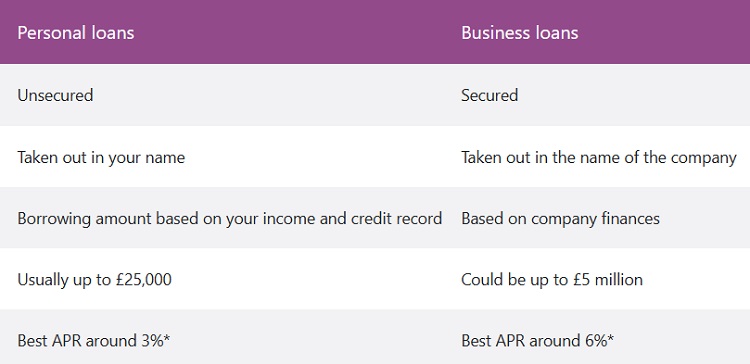

Use a Personal Loan to start a Business

Small- and medium-sized loans (SMEs) can benefit greatly from the terms and conditions of business loans. However, getting a business loan can be challenging because most lenders need at least two years of financial statements.

A personal loan could be used to launch a business in the absence of a traditional business loan.

Lenders typically require applicants to specify the purpose of the loan, so you may want to confirm that business startup is a legitimate reason before applying for a personal loan. If you don’t, they might turn down your offer.

New firms can also take advantage of specially tailored business loans.

The risks of using a Personal Loan for a Business

A business personal loan will be opened under your name. To put it another way, if the business doesn’t produce enough money to make the payments, you will be held personally liable for them.

Not paying them on time could hurt your credit score. The possibility of future credit access is diminished.

Can You apply for a Peer-to-Peer Loan?

While P2P loans are still a newer kind of business financing, they have become a popular choice for individuals in need of quick cash.

A lender or investor provides money for a business, allowing it to expand. It could be a single generous money or a group of people who each chip in a little.

Similar to a traditional bank loan, the lender receives interest on the business they loan to small businesses, and the businesses then repay the money they borrowed plus interest. In many cases, this is a better option than going to a bank for firms in need of financing.

There are, however, concerns for borrowers to consider, such as the fact that not all P2P lending is insured by the Financial Services Compensation Scheme just yet (FSCS).

This means that if the P2P lending network fails, borrowers may have a hard money recovering their funds. Most P2P networks, however, employ security precautions to prevent this from happening.

How much can I borrow with a Business Loan?

With a business loan, you may normally borrow anything from £1,000 to £3,000,000. But it depends on the state of affairs and the credit of your company. Both the type of business loan you acquire and the length of time you choose for repayment will play a role.

Think about your options if your financial situation were to alter and whether or not you would still be able to afford the payments.

Should I get a short-term or long-term Business Loan?

The health of your business’s finances will determine how long you have to make loan payments.

Lower interest rates and lesser monthly payments are typical of loans with longer payback terms. However, the lengthier repayment period will result in higher interest charges. Your ability to make ends meet each month can also be affected.

Long-term loans are more difficult to secure because lenders have more reason to worry about how your finances will evolve over the loan’s lifetime.

What information and documents need to apply?

The money you are requesting, as well as its intended use, must be disclosed to the lending institution. Get together the required paperwork before submitting your application. These might include:

- Business bank statements

- Financial statements

- Business tax returns

- Personal tax returns

- Any other legal documents

- Company director proof of address and IDs